If the crypto industry is compared to a set of teeth, the path of listing over the years is like a process of "industry orthodontics." From the chaos of 2017 to the industrialized assembly line of 2025, every method of token distribution is essentially a correction of the industry's structural deformities and a challenge to the chip structure.

In this process, the path for projects to pursue top liquidity has evolved from the early "volume game" to the current "sky-high bride price model" of spending heavily to win over; exchanges, for survival, traffic, and fees, have also shifted from early listing logic to pricing logic.

How exchanges, projects, VCs, and traders destroy and love each other; slander and achieve each other.

For you, a thousand times over.

Introduction

Teeth are a very "magical" organ in the human body. Why is that? Because teeth are the only organ that allows us to undergo deep customization, movement, and transformation through physical and biological means after adulthood.

This "plasticity" allows us to combat misalignment caused by genetics and the wear and discomfort brought by time.

We usually think of bones as hard and fixed, and teeth, growing in the alveolar bone, should be immovable. But orthodontics (wearing braces)恰恰利用了 the characteristic that bone is a "dynamic and active tissue." When braces apply a constant light force to the teeth, the alveolar bone on the pressured side senses the pressure, and the body sends "osteoclasts" to absorb the bone here, making way for the teeth; on the side where the teeth move away, the body sends "osteoblasts" to fill in new bone.

Teeth "destroy" bone on one side and "rebuild" it on the other,从而实现 slow movement within the bone.

This is something no other hard organ in the human body can do. After all, unless you are extraordinarily gifted, you cannot shorten your femur or change the position of your ribs by applying pressure, but teeth can.

The rules and policies of listings are the same.

Part One: Listing = The Struggle and Transfer of Asset Pricing Power

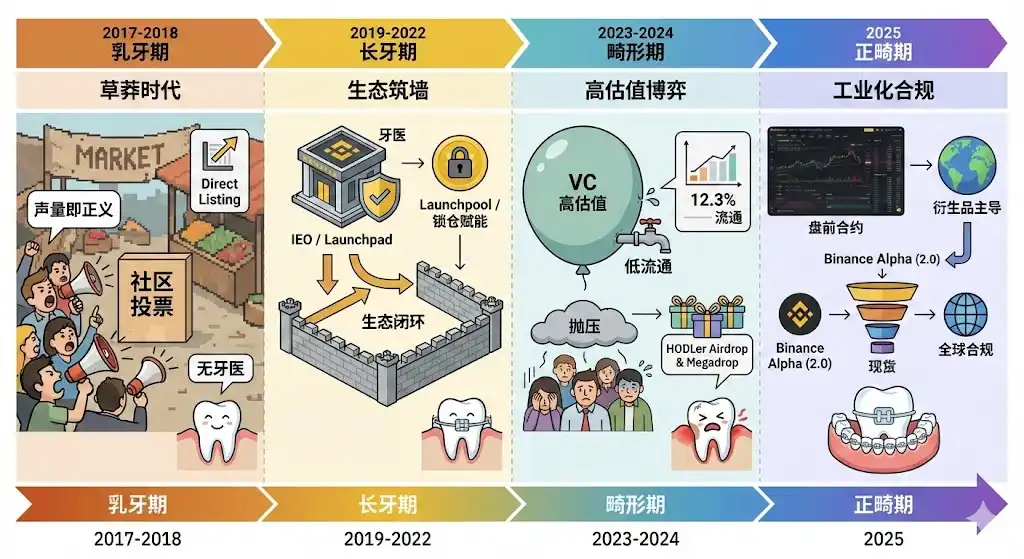

This article divides the path of listing into four stages: Baby Teeth — Growing Teeth — Deformity — Orthodontics. The core running through the four evolutionary stages of listing is: who masters the pricing power of assets.

Stage One (Community Pricing)

Pricing power lies in the hands of "shouters" and grassroots communities. Traffic is king, whoever has the loudest voice is right. The result is bad money driving out good, and the market is full of noise.

Stage Two (Exchange Pricing)

Exchanges reclaim pricing power through IEO/Launchpad, acting as "gatekeepers" and "investment banks." The exchange's credibility背书 becomes the core support for asset prices.

Stage Three (The Collapse of VC Pricing)

VCs掌握了 too high pricing power in the primary market, leaving no profit in the secondary market. Exchanges are forced to intervene, trying to "rob the rich to help the poor" through强制手段 (Airdrop), but this is only a painkiller, not a cure.

Stage Four (Market/Derivatives Pricing)

On-field博弈 funds are not in spot trading, so pricing power is handed over to more mature financial mechanisms. Through "contract trading" and pre-market trading, the market forms a fair price after full博弈, no longer relying on a single narrative or VC valuation reports.

Part Two: The Era Background, Logic, and Evolution of Listings

Stage One: 2017-2018 "Baby Teeth Period" — The Lawless Era Where Volume Was Justice

Core Path: Direct Listing, Community Voting

The industry was in a "no dentist" state during this period. The listing logic had a strong founder and community sovereignty color. As long as a project could rally fans, it could get an entry ticket.

Era Background

This was the "Genesis" stage of Crypto. The industry was still in a pure trading platform era, with users mainly concerned with convenience, speed, and low cost of trading. Mainstream exchanges at the time were mostly slow and unstable. New platforms built口碑 through "extreme simplicity," with no complex learning systems or social functions, and interfaces designed entirely for experienced professional traders.

Reasons

Customer Acquisition Anxiety: Startup platforms needed to attract traffic from competitors efficiently and at low cost. "Community voting" was not just about selecting coins but also a battle for community归属感.

Regulatory Vacuum: Global regulation had not yet intervened, giving exchanges extremely high decision-making freedom. The logic was极其简单: whichever project had the most fans was the guarantee of liquidity.

Play: Represented by Binance's "Monthly Community Vote Listing," users paid a tiny amount of tokens (e.g., 0.1 BNB) to vote. Winning projects (e.g., Zilliqa, Pundi X) almost got top流量 for free, but also led to severe market misalignment due to vote manipulation, eventually forcing its abandonment.

Stage Two: 2019-2022 "Teeth Growing Period" — Ecosystem Wall-Building and Premium Issuance

Core Path: IEO (New Coin Offering), Launchpad, Launchpool, Direct Listing

The industry began to wear an orthodontic appliance called "ecosystem." Exchanges were no longer just intermediaries but became "dentists" with deep due diligence capabilities.

Era Background

After the ICO bubble burst in 2017, fraud and technical vulnerabilities left the industry信用扫地. The market needed a safer,背书的 way to raise funds. Meanwhile, the arrival of DeFi Summer (2020) made "liquidity mining" an industry consensus.

Reasons

Credit Repair: Exchanges introduced "bank-level" due diligence through Launchpad, acting as industry dentists,筛选 serious teams and tech projects, upgrading the ICO model to the more secure IEO (Initial Exchange Offering).

Ecosystem Loop: To consolidate user stickiness, platforms forced value accrual to their own ecosystem coins (e.g., BNB) through Launchpool, allowing users to obtain new coins by "holding" rather than "snatching," reducing participation risk.

19-20 (New Coin Frenzy):

Launchpad (e.g., Bittorrent) introduced a pricing issuance model. Projects not only had to pass technical review but also accept the exchange's pricing "suggestions" to ensure some "wealth effect" after listing.

21-22 (Lock-up Empowerment):

Launchpool became mainstream, empowering platform tokens, marking a shift from "buying new coins" to "mining new coins." Users obtained new coin distributions by locking up platform tokens,强行 binding project利益 to the platform ecosystem.

Stage Three: 2023-2024 "Deformity Period" — High Valuation, Low Float博弈 and Mechanism Upgrade

Core Path: HODLer Airdrop, Launchpool

Era Background

Venture capital (VC) returned to the market on a large scale,催生 a large number of projects with valuations of hundreds of millions of dollars but extremely low listing float (median only 12.3%). This structure left little profit space for retail investors in the secondary market, only continuous unlock selling pressure. Meanwhile, paying huge fines and CZ going to jail shifted the focus from "wild growth" to "global compliance and stability."

Reasons

Pricing Power Conflict: VC-driven projects peaked at listing, depriving the market of price discovery功能. To protect the ecosystem, exchanges had to correct this through强制手段, "returning profits to the people."

Compliance Pressure: Starting May 2024, rules clearly favored small and medium-sized projects with high distribution ratios, requiring projects to reduce the float portion, aiming to打击 VC manipulation of pricing.

Corrective Measures: Introduced HODLer Airdrop and Megadrop targeting long-term holders,强行 giving the "bride price" directly to retail.

This is the most painful "periodontitis" stage of industry orthodontics. VCs催生大量 "peak at listing" projects, with token float median dropping to 12.3%. Binance's industry report showed that仅2024's new projects had about $155 billion in potential selling pressure over the next 12-24 months.

Because VC manipulated pricing, retail bought high, listing was the peak, causing a暴跌 in market confidence. Poor secondary market performance led to萎缩 in spot trading volume.

To maintain platform token attractiveness,引流, and trading demand, platforms began大规模推行 HODLer Airdrop (airdrops for long-term holders) and Megadrop (distribution combined with Web3 tasks). Listing policies gradually tilted towards small and medium-sized projects with high distribution ratios.

Starting in the second half of 2024, exchange contract mechanisms underwent major upgrades,开始 supporting a wider range of small-cap and new coin perpetual contracts, allowing risk hedging and early pricing through derivatives before spot liquidity matured. Exchange traffic and revenue sources also shifted towards perpetual contract trading.

Stage Four: 2025 "Orthodontics Period" — Multi-tiered, Industrialized Compliance Matrix

Core Path: Binance Alpha Airdrop, Pre-Market Trading, Web3 Wallet integration

Era Background

2025 is called the "Year of Crypto Industrialization." Total digital asset market cap突破 $4 trillion, Bitcoin became a macro asset. Perpetual contracts have become dominant in the derivatives market, accounting for over 75% of global crypto derivatives trading volume.

Reasons

Pricing Power Change: The market is no longer driven by narratives and shouting, but by ETF flows, corporate earnings, and protocol revenue.

Efficiency Optimization: Pre-market contract trading (Futures First) allows pricing through derivatives before new coins list on spot. 2025 data shows this path's conversion cycle shortened to 14 days, the fastest通道 into the mainstream.

Pre-Market Futures First: This is the most important mechanism change in 2025. Introduced "Pre-Market Trading," allowing users to trade perpetual contracts with up to 5x leverage based on external price feeds before the token is officially listed on the spot market.

Small-Cap Deep Liquidity: Because contract trading and pre-market trading attracted huge traffic, it attracted many small and medium market makers, greatly enhancing the博弈 space and liquidity of small-cap contracts. This allowed new coins like ESP, AZTEC, KITE, which had not yet listed on spot, to quickly establish derivative liquidity, becoming the fastest path into the mainstream, with an average cycle from listing to正式发币 of about 14 days.

Binance Alpha (2.0): As a "pre-listing token selection pool," projects must first "level up" here, proving their secondary market performance (including price trends and trading volume), to gradually upgrade: contract → spot.

Part Three: The Shift of Power from "Lawless" to "Industrialized Orthodontics"

Stage One: The Lawless Era of "Volume is Justice" (2017-2018)

This was the "primitive accumulation" period for exchanges. They had almost no ability to discern project quality, nor did they need to. They only needed to answer one question: "How many new users will listing this coin bring me?"

This model cultivated the first batch of "profit-only" crypto users, loyal to neither platforms nor projects, going wherever there was meat, sowing the seeds for the later liquidity mining tragedy.

Stage Two: The "Ecosystem Wall-Building" Teeth Growing Period (2019-2022)

Exchanges reached the peak of power, becoming the top of the food chain. They were not just trading venues but became super nodes integrating broker, investment bank, and regulator. IEO was the best tool for exchanges to monetize their brand premium.

Stage Three: The阵痛 of the "Deformity Period" (2023-2024)

This was a backlash against the overexpansion of VCs in the previous bull market. High FDV, low float projects were essentially institutionalized harvesting of retail by VCs using information asymmetry and capital advantage.

The aforementioned "$155 billion potential selling pressure" is an astonishing number. It explains why the altcoin market was lifeless even as Bitcoin hit new highs. Because the market not only lacked new funds but was also constantly being drained by unlocks from old projects.

This shows the helplessness of exchanges:明知 they are pits, they still have to list new ones to maintain competitiveness. Megadrop and HODLer Airdrop seem innovative but are actually defensive measures where exchanges are forced to "tax" VCs and subsidize users to maintain ecosystem activity. This is a painful "stock game."

Stage Four: The Industrialized Future of the "Orthodontics Period" (2025 Outlook)

In this stage, the industry finally realized that relying solely on spot markets and simple IEOs, airdrops, and KOL rounds could no longer bear the increasingly complex capital demands and community pressures.

In this stage, contracts replace spot as the primary means of price discovery, along with pre-market trading.

First, this is a huge paradigm shift. It used to be "assets first, then derivatives"; the future is "derivatives博弈 pricing first, then spot asset delivery." This greatly accelerates the price discovery process. How much a project is worth doesn't need to wait for the暴涨暴跌 at listing; it is completed in advance through the long-short battle in pre-market contracts.

The emergence of Binance Alpha also provides a前置 window for "industrialized listing." Alpha is essentially a "talent show sandbox" or a "decentralized curated market." It requires projects to prove their liquidity and resilience in the real残酷 market before they can qualify for "promotion." This replaces the manual due diligence of Stage Two with market mechanisms.

Part Four: The Evolution of Listing Fees: From Listing Fee — Toll Money — Share Money

This section does not target any specific exchange, only叙述 based on public information..

The evolution of "listing fees" through these four stages is essentially a process of power transfer within the industry: from the initial "paying the platform toll money" to the current "spending the family fortune to娶 traffic." We can see how the industry has evolved step by step through this "bride price" perspective.